07.04.2026

Management-Defined Performance Measures (MPMs): From Voluntary to Regulatory Disclosure

One of the most significant changes introduced by IFRS 18 is the regulatory requirement to disclose management-defined performance measures (MPMs). What was previously a matter of voluntary disclosure is now a compliance requirement. This article examines the implications of this change and outlines how companies need to adapt their governance and reporting practices.

What are Management-Defined Performance Measures (MPMs)?

Management-Defined Performance Measures sind Leistungskennzahlen, die das Management eines Unternehmens extern kommuniziert, die aber nicht explizit durch IFRS definiert sind. Beispiele umfassen:

Management-defined performance measures are key performance indicators that a company’s management communicates externally but that are not explicitly defined by IFRS. Examples include:

Adjusted EBITDA: A measure of operating profitability that excludes depreciation, amortization, and financing costs and is often adjusted for non-recurring items.

Adjusted Operating Income: A measure of operating income that is adjusted for one-time items to show underlying operating performance.

Working Capital: A measure of short-term liquidity, calculated as current assets minus current liabilities.

Free Cash Flow: A measure of available cash flow after investments, often calculated as cash flow from operating activities minus capital expenditures.

Organic Growth: A measure of growth excluding acquisitions or divestitures.

Return on Invested Capital (ROIC): A measure of the profitability of invested capital.

These metrics are frequently used by companies in investor relations presentations, annual reports, and analyst conferences to communicate their performance.

The Shift: From Voluntary to Regulatory

Under IAS 1, MPMs were a matter of voluntary disclosure. Companies could decide which MPMs they wanted to disclose and how they calculated them. There were no uniform requirements for the calculation or the reconciliation to IFRS metrics.

This led to a situation where different companies calculated the same metric differently, making comparability difficult. For example, a company might calculate “Adjusted EBITDA” without taking acquisition costs into account.

IFRS 18 fundamentally changes this. Companies must now:

-

Disclose MPMs that they communicate externally: Any metric that management communicates externally must be disclosed in the notes.

-

Provide a reconciliation: For each MPM, a clear reconciliation to the new IFRS 18 subtotals must be provided.

-

Account for tax effects and effects on non-controlling interests: The reconciliation must account for all effects, including tax effects and effects on non-controlling interests.

-

Ensure consistency across multiple periods: The calculation of MPMs must be consistent across multiple periods.

-

Subject to the annual audit: MPMs are now subject to the annual audit by external auditors.

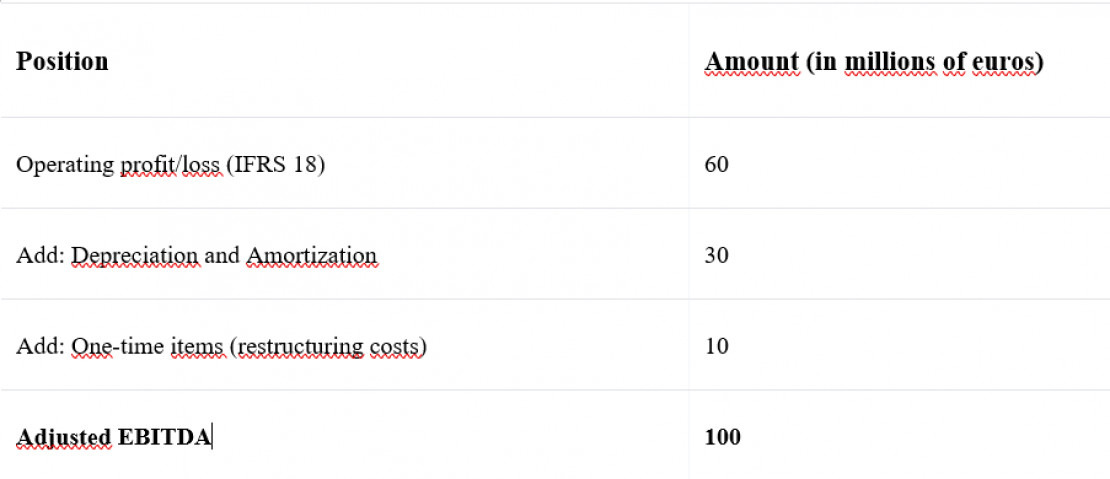

Practical example: Reconciliation of Adjusted EBITDA

To illustrate these requirements, let’s consider a practical example: the reconciliation of “Adjusted EBITDA” to the new IFRS 18 subtotals.

Suppose a company reports an “Adjusted EBITDA” of 100 million euros externally. The reconciliation might look like this:

The reconciliation outlined here is a simplified representation. In practice, reconciliations are often significantly more complex, particularly when tax effects and the impact on non-controlling interests must be accurately accounted for, which requires a detailed analysis.

“Adjusted EBITDA” has frequently been used as a voluntary disclosure in management reports or investor presentations, with these “non-GAAP measures” allowing for a certain degree of flexibility.

With the introduction of IFRS 18, this changes fundamentally: such metrics will in the future become a mandatory component of the audited notes as management-defined performance measures (MPMs). This marks a significant leap in compliance.

While adjustments were previously often made without detailed derivation, IFRS 18 now requires a strict reconciliation from an official IFRS subtotal, such as operating profit. Furthermore, the respective tax effects must be disclosed individually for each adjustment item (e.g., restructuring costs).

Selective “cherry-picking” of extraordinary items is effectively ruled out by the new audit requirement and strict consistency rules (changes must be justified and adjusted in the prior year).

The requirements of IFRS 18 in detail

IFRS 18 sets out specific requirements for the disclosure of MPMs:

1. Identification of MPMs

-

Entities must first identify which performance measures are MPMs. This includes:

-

Performance measures used in investor relations presentations

-

Performance measures used in annual reports

-

Performance measures used in analyst conferences

-

Key figures used in press releases

-

Key figures used in guidance or forecasts

This is a broader definition than many companies have previously assumed. Many companies will find that they must disclose more MPMs than they have in the past.

2. Calculation and consistency

Companies must ensure that MPMs are calculated consistently. This includes:

-

Consistent definition of the components of the MPM

-

Consistent treatment of one-time items

-

Consistent treatment of acquisitions and divestitures

-

Consistent treatment of currency effects

3. Reconciliation to IFRS subtotals

For each MPM, a reconciliation to the new IFRS 18 subtotals must be provided. This reconciliation must:

-

Clearly present all adjustments

-

Take tax effects into account

-

Take effects on non-controlling interests into account

-

Be transparent and understandable

4. Notes

Companies must explain why they use the MPM and how it is relevant to users of the financial statements.

Governance and Audit Compliance

The requirement to disclose MPMs with complete supporting documentation has significant implications for governance and audit compliance:

Governance Requirements

Companies must establish governance processes to ensure that:

-

MPMs are correctly identified

-

MPMs are calculated consistently

-

Reconciliation statements are accurate

-

MPMs are subject to the annual financial statement audit

This often requires collaboration between various functions:

-

Investor Relations: Identifies which key performance indicators are communicated externally

-

Controlling: Calculates the MPMs and prepares reconciliation statements

-

Financial Accounting: Ensures that the data is accurate

-

Audit: Reviews the MPMs and reconciliation statements

-

Legal Department: Ensures that disclosures comply with requirements

Audit-proofing

The reconciliation statements must be audit-proof. This means:

-

The calculations must be documented

-

The data sources must be traceable

-

The calculation logic must be transparent

-

Changes must be traceable

This often requires the implementation of systems and processes that support audit compliance.

Practical challenges

Challenge 1: Identifying All MPMs

A practical challenge is identifying all MPMs that management communicates externally. This requires a thorough review of all external communication channels.

Solution: Establish a process in which all functions that communicate externally (Investor Relations, Marketing, Executive Management) regularly document all key performance indicators used.

Challenge 2: Consistency Across Organizations

Another challenge is ensuring consistency across different organizations, particularly in conglomerates with many subsidiaries.

Solution: Develop detailed guidelines for calculating MPMs and clearly communicate them to all organizations.

Challenge 3: Tax effects and effects on non-controlling interests

Accounting for tax effects and effects on non-controlling interests in reconciliation statements can be complex.

Solution: Work closely with your tax professionals and auditors to ensure these effects are accounted for correctly.

Challenge 4: System Support

The efficient calculation and seamless tracking of management-defined performance measures (MPMs) requires robust system support.

Particularly in the context of technical implementation in environments such as SAP S/4HANA or in group reporting, it becomes clear that MPMs can no longer be treated as isolated “Excel side calculations” at the end of the consolidation process.

Instead, they must be embedded as an integral part of the reporting structure. This ensures the transparency and audit compliance required by auditors at the click of a button.

The implementation of specialized systems such as SAP Analytics Cloud, Hyperion, or OneStream is therefore essential to ensure the precise capture and tracking of MPMs and to meet new compliance requirements.

Best Practices

Best Practice 1: Early Identification

Identify all MPMs that you are required to disclose at an early stage. This will give you sufficient time to implement governance processes and systems.

Best Practice 2: Clear Guidelines

Develop clear guidelines for the definition, calculation, and disclosure of MPMs. These guidelines should cover all aspects, including the treatment of one-time items, acquisitions, and currency effects.

Best Practice 3: Regular Review

Regularly review (at least annually) whether your MPMs are still relevant and whether new MPMs need to be added.

Best Practice 4: Close Collaboration with Auditors

Work closely with your auditors to ensure that your MPMs comply with the requirements of IFRS 18.

Best Practice 5: System Support

Implement systems that support the calculation, tracking, and disclosure of MPMs. This improves efficiency and reduces errors.

To meet the new requirements for audit trail integrity and transparency, companies should no longer manage MPMs as manual “top-side adjustments” in Excel. A best practice is to integrate the reconciliation directly into SAP S/4HANA Finance or SAP Group Reporting, for example:

-

Clear account or transaction type logic: Use specific statistical accounts or sub-items to clearly identify adjustments (e.g., restructuring costs) at the time of entry.

-

Automated reconciliation: Map the MPM logic directly to the Financial Statement Versions (FSV) or reporting hierarchies. This allows the reconciliation from operating profit to adjusted EBITDA to be generated at the click of a button with a full audit trail.

Conclusion: MPMs as a Strategic Governance Issue

The transition to IFRS 18 makes MPMs a strategic governance issue. Companies that systematically identify, calculate, and disclose their MPMs will not only ensure compliance but also improve their communication with investors and other stakeholders.

Investing in robust governance processes and systems for MPMs is an investment in the company’s credibility and transparency.