21.04.2026

Cash Flow Statement under IFRS 18: New Structure, New Logic

The transition to IFRS 18 affects not only the income statement but also the cash flow statement. IFRS 18 introduces changes to the structure and logic of the cash flow statement that impact reporting and liquidity analysis. This article examines these changes and explains how companies need to adjust their cash flow statements.

The previous structure of the cash flow statement

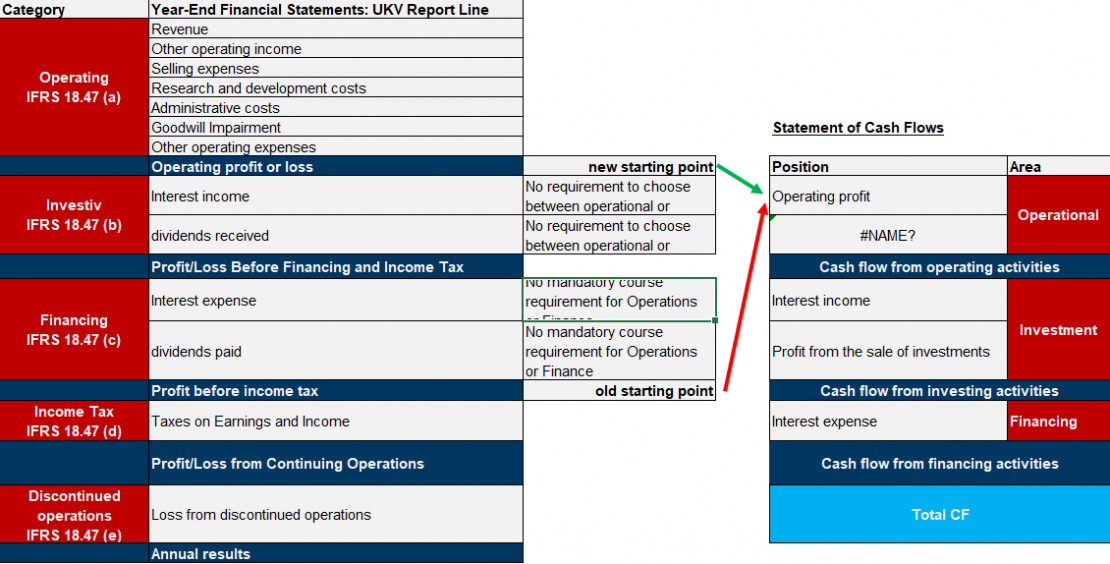

The statement of cash flows under IAS 7 is divided into three sections:

Cash flows from operating activities: Cash flows arising from the entity’s ordinary course of business.

Cash flows from investing activities: Cash flows arising from investments in assets and investments in other entities.

Cash flows from financing activities: Cash flows arising from financing activities such as borrowing or issuing shares.

This structure has remained essentially unchanged since the introduction of IAS 7 in 1992. It provides a clear distinction between the different types of cash flows.

The changes under IFRS 18

IFRS 18 introduces two significant changes to the statement of cash flows:

Change 1: New classification of interest and dividends

Under IAS 7, entities had discretion regarding the classification of interest and dividends.

Interest paid could be classified either as a financing activity or as an operating activity. Interest and dividends received could be classified either as an investing activity or as an operating activity.

IFRS 18 eliminates these options. The new rule is:

- Interest paid: Financing activities

- Interest received: Investing activities

- Dividends paid: Financing activities

- Dividends received: Investing activities

There are exceptions for companies whose primary business activities lie in these areas (e.g., banks, insurance companies), but for most companies, the classification is now clear-cut.

Change 2: Operating Profit/Loss as the New Starting Point

Under IAS 7, the starting point for determining cash flow from operating activities using the indirect method was profit before tax. Under IFRS 18, the new starting point is operating profit/loss—one of the new subtotals introduced by IFRS 18. This is a significant difference, as operating profit/loss does not include all financing costs and taxes.

Practical example: Restatement of the cash flow statement

To illustrate the impact of these changes, let’s look at an example.

Conclusion: Due to the stricter categorization of investing and financing activities within the income statement, certain accounting choices are no longer applicable, as these activities are now clearly separated from operating profit. Operating cash flow may be lower, while cash flows from investing and financing activities may be higher.

Impact on liquidity analysis

These changes have implications for liquidity analysis and the interpretation of the statement of cash flows:

Impact 1: Operating cash flows may appear lower

Since interest income and gains on investments are no longer included in operating cash flows, operating cash flows may appear lower than before. It is important to understand this, as it does not mean that operating performance has deteriorated—it is merely a matter of classification.

Impact 2: Investing cash flows may appear higher

Since interest income and gains from investments are now included in investing cash flows, investing cash flows may appear higher than before.

Impact 3: Comparability with Previous Years

When comparing figures with previous years, it is important to note that the classification may differ. Companies must reclassify prior-year figures to ensure comparability.

Challenges in Implementation

Challenge 1: Identifying All Affected Items

A practical challenge is identifying all items affected by the new classification rules. This requires a thorough review of all cash flows.

Solution: Create a detailed list of all items related to interest, dividends, or gains from investments, and review how these should be classified under IFRS 18

Challenge 2: System adjustments

The cash flow statement is often calculated in systems (e.g., SAP, group reporting systems). These systems must be adjusted to reflect the new logic.

Solution: Work with your IT teams to adjust the systems. This may involve adjusting calculation logic, account mappings, and reporting tools.

Challenge 3: Retrospective Application

The requirement for retrospective application means that companies must reclassify the 2026 cash flow statement.

Solution: Start planning and implementation early to allow sufficient time for adjusting historical data.

Best Practices

Best Practice 1: Early Planning

Plan the transition of the cash flow statement well in advance. This gives you time to adapt systems and establish processes.

Best Practice 2: Detailed Documentation

Document in detail how items are classified under IFRS 18. This helps ensure consistency and facilitates communication with auditors.

Best Practice 3: Review with Auditors

Review your classifications with your auditors to ensure they meet the requirements of IFRS 18.

Best Practice 4: Communication with Stakeholders

Clearly communicate the changes in the cash flow statement to stakeholders, particularly investors and analysts. This helps avoid confusion and improves comparability.

Best Practice 5: Impact Analysis

Conduct a detailed analysis of the impact of the transition. This helps identify potential issues early on.

Impact on different types of businesses

Banks and Insurance Companies

Exceptions apply to banks and insurance companies. Since their primary business activity involves the management of financing and investments, they may continue to include interest and dividends in operating cash flow. It is important to understand this, as it means that the cash flow statement for these companies looks different.

Manufacturing Companies

For manufacturing companies, the transition is relatively straightforward. Interest expenses are classified as financing activities, while interest income and gains from investments are classified as investing activities.

Retail and Service Companies

For retail and service companies, the transition is also relatively straightforward.

Conclusion: An important but manageable transition

The transition of the cash flow statement to IFRS 18 is a significant change, but it is manageable. Companies that plan early and systematically adapt their systems and processes will be able to successfully complete the transition.

The new structure of the cash flow statement also offers advantages: it is clearer and more consistent, and it eliminates accounting choices that led to comparability issues.